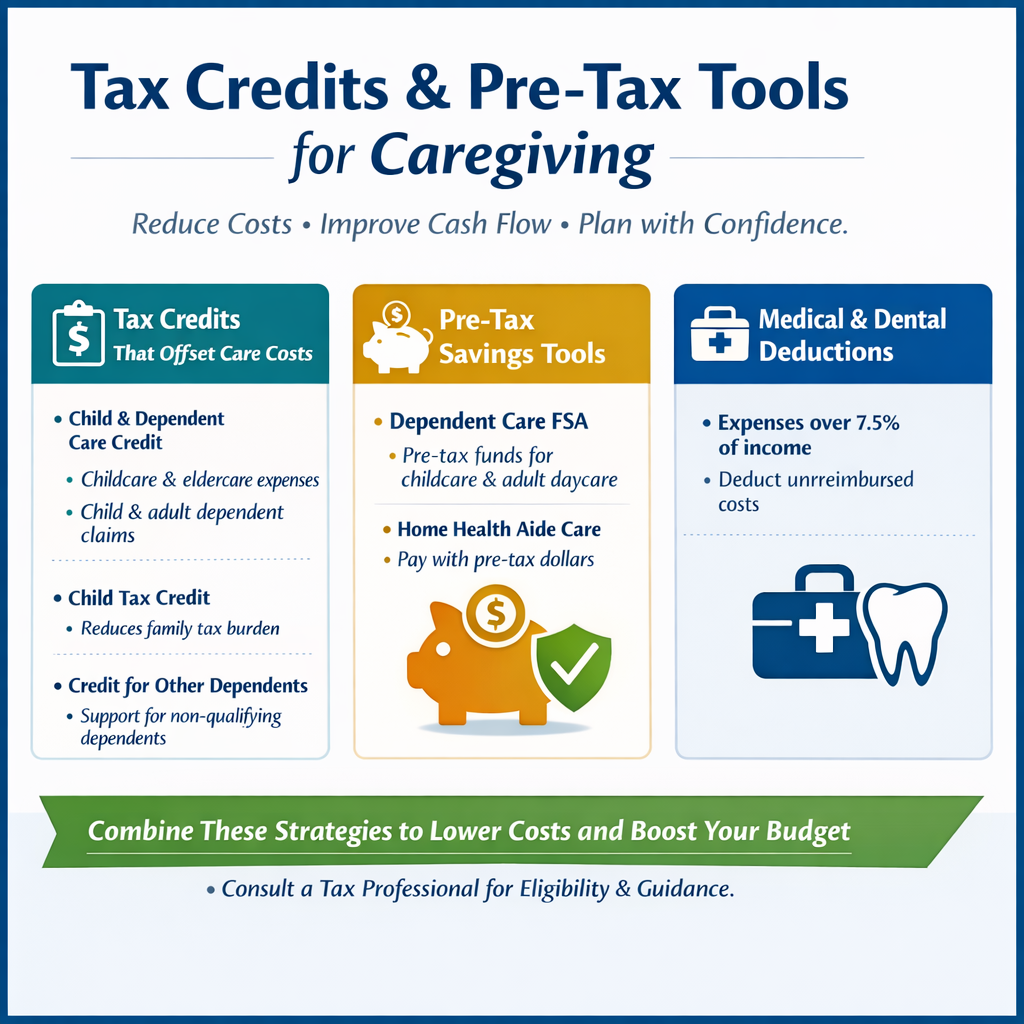

Understanding the Financial “Squeeze”

What makes this stage so challenging isn’t simply the cost—it’s the convergence of financial demands. Rising childcare, education, healthcare, housing, and long-term care expenses often overlap at the same time.4

As a result, many caregivers find themselves making difficult trade-offs—cutting back on work hours, delaying retirement contributions, or relying more heavily on savings and credit.3

This “squeeze” can feel overwhelming. But with thoughtful planning and access to the right resources, families can begin to regain a sense of control. In part one of this two-part series, we cover the first three of seven strategies for managing dual caregiver expenses.

1. Start with a Clear Financial Plan

The first step is clarity. Understanding your full financial picture—including income, savings, debt, and long-term goals—provides the foundation for every decision you make.

If possible, have an open conversation with your parent indicating that you will be assisting to determine what resources they have available to provide for their own care. If you will be helping them with financial and medical care decisions, they should consider naming you as a power of attorney who is authorized to act on their behalf if they become incapacitated.

From there, creating a dedicated caregiving budget that separates child-related and eldercare expenses from your other expenses can help you monitor costs and prepare for future needs.

Equally important is setting realistic expectations. Many caregivers feel pressure to meet every need—often at the expense of their own financial security. ³ Thoughtful stewardship means balancing generosity with sustainability.

2. Reduce Childcare Costs with Creative and Public Options

Childcare is often one of the largest expenses families face—but there are ways to manage it more effectively.

Nanny Shares

A growing number of families who use babysitters are turning to nanny shares, where two or more households share the cost of a caregiver. This arrangement allows families to:

- Split wages and payroll costs

- Maintain a more personalized, in-home setting

- Reduce overall expenses compared to hiring a full-time nanny independently

Nanny shares offer a practical way to balance quality care with affordability.

Free or Low-Cost Pre-K Programs

Some states and municipalities offer public pre-K programs, often at low or no cost depending on eligibility. These programs provide:

- Early childhood education

- Care during working hours

- Additional support services such as meals.

For families with young children, these programs can reduce annual childcare costs.

Next

Next